Share this

by Admin

Open banking provides consumers with control over their financial data, but it also equips financial institutions with a unique opportunity to share data with one another.

In other articles, we discussed the importance of a streamlined consumer experience, as well as why it’s vital to institute a supportive environment for your consumers.

Today, we want to address the topic of open banking – what it is, what it means for your current vendor integration technology and whether an open banking business model is a good fit for your organization and your consumers.

Making Open Banking Achievable For Traditional Community Financial Institutions Using APIs

Beginning in Europe with the European Union’s Payments Services Directive 2 (PSD2) in 2018, open banking ended an era of consumers being unable to transfer their data between financial institutions and services. It paved a way for the highly competitive landscape of FinTechs that we see today.

Financial institutions may find open banking to be the ‘villain’ of their business’s story, especially with the rise of so many challenging neobanks. 29% of banking’s traditional retail-based revenue streams are at risk. But this traditional mindset will be what breaks or makes the future of financial institutions as we know them.

“The truth is that the future is digital,” explained Dan Shehan, the Digital Strategist at FTSI, “and the future of digital is open banking. To be at the forefront, financial institutions need to think about more than money. What other value, financial advice or tools can your FI provide? How can you highlight the trust your FI has earned – something many Fintechs lack?”

Some financial institutions have taken a progressive approach of partnering with FinTechs, instead of running up against them. Open banking allows that partnership to form and be profitable, as well as for the consumer.

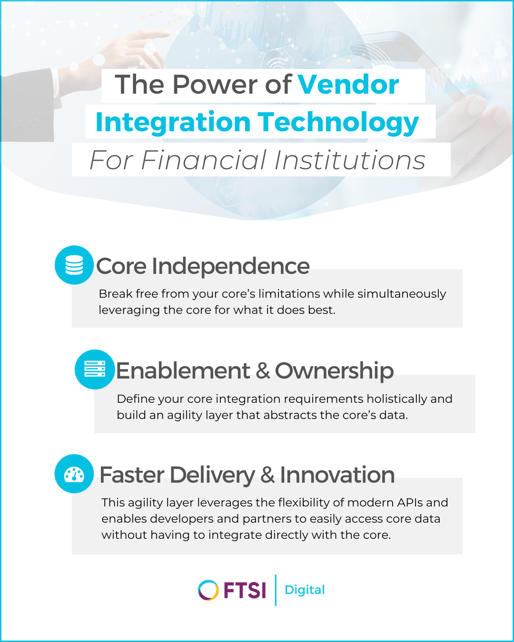

Others wish to re-engineer their backend for digital, which would also provide an opportunity to explore open banking – but it certainly comes with its setbacks, like cost and core integration.

“This is where APIs come into play,” said Dan. “Open banking is fast, secure and standardized. By using APIs that are well-understood in the industry, consumer data can be moved to where it needs to be, in real-time, with ease. It enables FIs to remain agile, make changes and try things out in their ecosystem that, in a traditional method, would be very costly and take a lot of time to achieve.”

A scalable, open API platform in the cloud will allow you to make a smoother, cost efficient transition to digital and open banking. Think about APIs like a modular power strip -- one you can customize to have any kind of sockets you want.

Your partnerships with vendors and third-party technologies are what will ‘plug-in’ to your power strip.

Unlike traditional core integration, you won’t have to go through the often lengthy and costly process of ‘disconnecting’ or ‘connecting’ a new relationship to your core. Instead, you can simply ‘plug’ or ‘unplug’ the connection without it affecting any of the other connections you may have.

“The other HUGE differentiator with APIs in the cloud is being able to have your data on as many servers as necessary across a global network. You have active, active backup – two instances where your data is working. Your data isn’t hosted on physical servers,” explained Dan.

Related: Super Apps Are Shaking Up the Banking Industry

Let’s say your organization operate out of California, and perhaps you’ve always had your physical servers also located in California. If something were to happen to California tomorrow (or even just the place your server is located), then you would lose access to your data. Your organization is suddenly in the hands of where your server is located.

With a cloud-based API platform, the power is put back in your hands – not only from a vendor partnership perspective but also from a security standpoint. It’s sustainable, flexible, and it can evolve as your organization evolves. Plus, more than 50% of banking organizations will not use core providers for open banking solutions due to this flexibility.

“Imagine being able to work with anybody you want,” said Dan, “regardless of whether or not it’s supported by your core provider or third parties.”

Who Is Open Banking Best For?

“There isn’t a financial institution out there that couldn’t benefit from this technology,” Dan said. “There’s enough red-tape to get through these days. Open banking provides this unique opportunity to truly reinvent your business model in a way that works for you, rather than against you.”

The landscape is competitive – and that won’t change. If anything, more and more neobanks will pop up, especially as more consumers lean toward new incentives. Financial institutions must find a way to embrace the future of digital, and taking advantage of the opportunities open banking and scalable API, cloud-based platforms provide is a fantastic place to start.